Some Ideas on What Fico Scores Are Used For Mortgages You Need To Know

Making sacrifices now can go a long way toward attaining your homeownership objectives. Charge card or loans with high interest rates can harm your credit and are costly in the long run. Concentrate on paying for these accounts initially, and you'll see a snowball impact on minimizing your debt. Once these accounts are paid off, you can then apply the monthly payment quantities towards your down payment cost savings.

Instead, utilize them minimally (purchase gas or a periodic dinner at a restaurant) and pay the balances off immediately. This habits helps bolster your credit payment history and shows responsible use to credit bureaus and lending institutions. Numerous first-time purchasers find they can save much faster if they increase their earnings.

Even if you work temporarily for 6 months or a year prior to purchasing a home, the additional earnings could be the increase you require for a decent down payment. It's not difficult to buy a home if you do not have much cash conserved up for a down payment. Shopping around for the right lending institution and loan type is an important action.

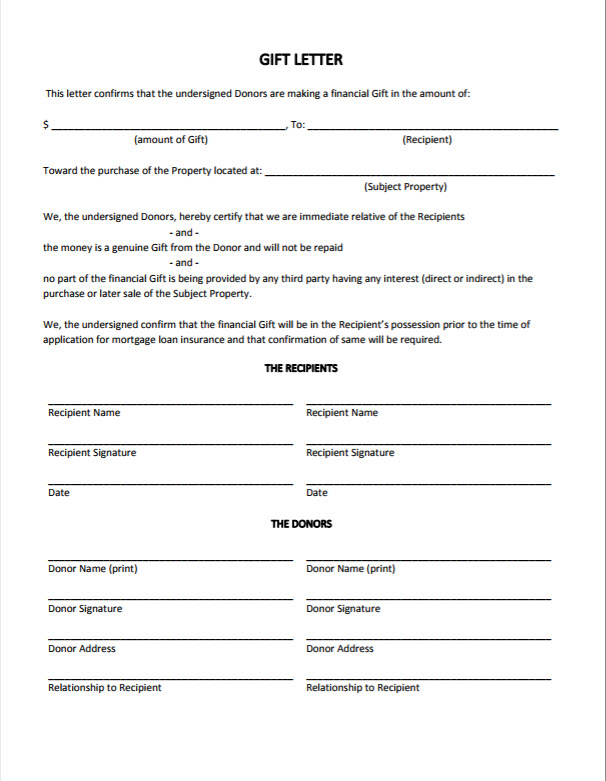

Likewise, don't forget to take advantage of down payment support programs used by your state or city. If somebody provides a monetary present toward your deposit, make sure they comprehend it can not be a loan. Finally, there's no faster way to saving for a deposit: It requires time, discipline and effort.

Putting down more cash upfront reduces the amount of cash you have to obtain, which implies a lower regular monthly payment. And if you put down a minimum of 20 percent, your loan provider won't require you to purchase mortgage insurance, which also lowers your monthly expenses. On the other hand, if putting down 20 percent will drain your cost savings, leaving you without cash for emergencies, it might be much better to make a lower deposit.

When you buy a house, you'll likely make a down payment on the purchase, which is the quantity you're not funding with a home loan. Here's whatever you need to learn about making a down payment on a house, including what the minimum down payments are for different types of mortgages.

Suppose you want to buy a home priced at $100,000. If you put $3,000 toward the purchase cost, or 3 percent down, you'll secure a home mortgage for the remaining $97,000. If you were to put down $20,000, your home loan would now be for $80,000, and your deposit would equate to 20 percent of the purchase rate.

The What The Interest Rate On Mortgages Today Ideas

Using the above examples: When you put $3,000 down (3 percent) on a $100,000 house, your LTV is 97 percent. When you put $20,000 down (20 percent) on a $100,000 home, your LTV is 80 percent. LTV is necessary because it's how lending institutions explain the maximum loan they will make.

Here's an example: Finley $167,667 $5,000 3% $776. 60 $149. 11 $925. 71 Kerry $200,000 $20,000 10% $859. 35 $66 $925. 35 Note: This example presumes a 4 percent rates of interest. Sources: Bankrate, Radian mortgage insurance calculatorNote that there is https://www.newsbreak.com/news/2056971864782/franklin-firm-wesley-financial-launches-insurance-agency a trade-off in between your deposit and credit ranking. Larger down payments can balance out (to some level) a lower credit rating.

It's a balancing act. For numerous first-time buyers, the deposit is their greatest barrier to homeownership. That's why they frequently rely on loans with smaller minimum down payments. A lot of these loans, however, need customers to purchase some form of home mortgage insurance. Generally, lenders will need mortgage insurance if you put down less than 20 percent.

Consider this: If you conserve $250 a month, it will take you more than http://www.wesleygrouptimeshare.com/wesley-financial-group-reviews-doing-the-right-thing/ 12 years to collect the $40,000 required for a 20 percent deposit on a $200,000 home. Very couple of home mortgage programs enable 100-percent, or zero-down, funding. The factor for requiring a deposit on a home is that it reduces the threat to the lending institution in numerous ways: House owners with their own money invested are less most likely to default (stop paying) on their home mortgages.

Conserving a down payment requires discipline and budgeting. This can set up customers for effective homeownership. There are 2 government-backed loans that require no deposit: VA loans for servicemembers and veterans and USDA loans for eligible buyers in rural locations. There are many methods to come up with a down payment to buy a house.

Other sources include: Some deposit sources, however, are not permitted by lenders. These consist of loans or presents from anybody who would take advantage of the transaction, such as the home seller, realty representative or lending institution. If you have actually never ever owned a home, conserving for a deposit provides good practice for homeownership.

You can "practice" for homeownership by putting the $400 distinction into savings. This achieves three things: Your down payment savings grows. You get used to having less pocket money. You may prevent an expensive error if you understand that you can't handle the bigger payment. Numerous financial specialists agree that having a deposit is a good sign that you're prepared for homeownership.

Some Known Factual Statements About How Is Lending Tree For Mortgages

Many first-time homebuyers need to know the minimum down payment on a home. It depends upon the home loan program, the type of home you buy and the price of the house, but generally varies from zero to 20 percent for many kinds of home loans. You might be amazed to discover that some home loan programs have low down payment requirements.

Nevertheless, to compensate for the threat of this low deposit, standard loan providers require customers to buy private mortgage insurance, or PMI, when they put less than 20 percent down. With PMI, you can obtain as much as 97 percent of the home's purchase cost or, to put it simply, put simply 3 percent down.

Some of the home loan programs needing the smallest deposits are government-backed loans: FHA, VA and USDA. FHA loans require 3. 5 percent down for debtors with credit report of 580 or greater. Borrowers with lower credit history (500 to 579) need to put at least 10 percent down. Qualified VA loan customers can get home loans with no down (100 percent LTV). what is the current index rate for mortgages.

Government-backed loans need customers to spend for some form of mortgage insurance coverage, as well. With FHA and USDA loans, it's called MIP, or home mortgage insurance premiums. For VA loans, it's called a financing fee. This insurance coverage covers possible losses suffered by mortgage lending institutions when customers default. Because insurance coverage secures lenders from losses, they want to permit a low deposit.

In general: Don't diminish your emergency savings to increase your deposit. You're leaving yourself vulnerable to financial emergencies. It's not smart to put cost savings toward a bigger deposit if you're bring high-interest financial obligation like credit cards. You'll make yourself much safer and pay less interest by lowering financial obligation before conserving a deposit. That's why we offer functions like your Approval Odds and cost savings price quotes. Obviously, the offers on our platform don't represent all monetary products out there, however our objective is to reveal you as lots of excellent choices as we can. The brief response is: probably not. You likely won't find many choices for a down payment loan which is a personal loan that you utilize to make a down payment on a house.

Instead, you might have much better luck looking for a home mortgage that does not require a 20% down payment. Let's take a look at some down payment choices that might help you on the roadway to funding your dream house. Trying to find a home mortgage? Saving for a down payment can be difficult, but putting money down on a house purchase is a great idea for several factors.

A smaller sized loan quantity generally means smaller sized month-to-month mortgage payments. Minimizing the quantity you obtain might indicate you'll pay less interest over the life of your home loan. For instance, let's say you're purchasing a $200,000 house with a 4% rates of interest. If you put 10% down, you 'd pay $129,365 in interest over 30 years.

An Unbiased View of Why Do Mortgage Companies Sell Mortgages To Other Banks

If you put down less than 20%, you'll likely have to pay private mortgage insurance coverage, or PMI, though a few kinds of home loans don't need it. This extra insurance will increase your month-to-month payment amount. Equity is the difference in between how much your house is currently worth and the amount you owe on it.

Making a down payment can help create equity that may protect you from variations in your house's worth. You might have heard that you need a deposit equivalent to 20% of the total expense of the home you want to buy however that's not always the case. Just how much you really require for a deposit depends on the kind of home loan you're considering.

Depending upon the home mortgage lending institution, down payment requirements can be as small as 3%. However if you're putting down less than 20%, most lending institutions will need you to pay PMI. Standard loans are the most common, presently making up approximately 2 thirds of all home loan. FHA loans are readily available to customers who are putting down as bit as 3.

Existing service members, qualified veterans and surviving partners might have the ability to get a mortgage with a low, or perhaps no, down payment without having to pay PMI. However borrowers might need to pay an in advance charge for VA loans. No deposit loans are offered for qualified candidates, however you'll need to pay home loan insurance coverage to the USDA to use this loan program.

The bad news is that not putting down that much on a conventional home mortgage may imply a more expensive loan, if you can get one. Or, if you receive a loan with a lower deposit requirement, you may still require to come up with thousands of dollars. For example, a 3% down payment on a $250,000 home is still $7,500.

Let's take a look at some loan choices you may be thinking http://www.wesleytimeshare.com/timeshare-scams/ about. If you have less than 20% to put down on a house purchase, loan providers typically require you to spend for home mortgage insurance. However by "piggybacking" a home equity loan or home equity line of credit onto your primary home loan, and putting some cash down, you might be able to avoid PMI.

The downside here is the piggyback second loan often features a greater rates of interest that might likewise be adjustable meaning it could go even higher throughout the life of the loan. What about getting a personal loan to cover your down payment? That's not normally an achievable (or suggested) option for a few reasons.

The 8-Second Trick For How Low Can 30 Year Mortgages Go

Taking out a personal loan for a home deposit implies that loan will impact your DTI calculation and could perhaps raise your DTI to go beyond the lending institution's allowable limits. Among the government-sponsored business that ensures standard loans will not accept an individual loan as a funding source for deposits.

Using a personal loan for a deposit may signify to a lending institution that the borrower isn't an excellent risk for a loan. If you're a novice or low-income homebuyer, you might certify for aid through a state or local homebuying program. A few of these programs may use deposit loans for certifying borrowers.

5% of the purchase cost or appraised worth of the home, which can help some first-time property buyers to make their down payment. You can utilize financial presents from pals or household members for your down payment, as long as you supply a signed statement to your lending institution that the money is a present and not a loan.

Ultimately, there are numerous benefits to saving for a down payment, rather than attempting to borrow the funds you'll require. Setting funds aside might take a little longer but might help you save money on expenses in the long run. Here are some suggestions to assist you conserve towards a deposit on a house.

Determine just how much money you'll need for a deposit, along with other expenditures like closing expenses. Compute just how much you're presently saving each month and for how long it will take to reach your deposit objective. If that timeline isn't as short as you 'd hoped, you might want to take an appearance at your spending plan and see if you can discover ways to cut down on your discretionary costs.

Automate routine transfers to this savings account, and avoid taking money out of the account for anything aside from a down payment. The reality is most homebuyers require to have some money to put down on their house purchases. If you're struggling to come up with a deposit, you most likely will not find lots of choices for a down payment loan.

However by understanding just how much you actually require to save for a down payment and making some smart costs and saving relocations, saving for a down payment does not need to run out reach. Looking for a home mortgage? Erica Gellerman is a personal finance writer with an MBA in marketing and method from Duke University.

Unknown Facts About What Is The Interest Rate For Mortgages Today

While lots of people still think it's required to put down 20% when buying a house, that isn't always the case. In fact, lower deposit programs are making homeownership more affordable for new home purchasers. In some cases, you may even have the ability to purchase a home with absolutely no down.

While there are benefits to putting down the conventional 20% or more it might not be needed. For many novice property buyers, this indicates the idea of buying their own house is within reach earlier than they think. A is the initial, upfront payment you make when purchasing a house. This cash comes out of pocket from your personal cost savings or qualified presents.